The Plasma Blockchain

Built for Stablecoins, Launched with $2 Billion in Liquidity

Every once in a while in crypto, a new chain launches and you can feel the buzz. Most of the time, I’m skeptical. I’ve been around long enough to see dozens of brand-new chains spin up, attract early hype, and then fade as quickly as they appeared, or they make it but not without serious hiccups. They often bring new native DEXs and lending protocols that haven’t been tested, and the risk of exploits is much higher. So my default reaction is mostly to avoid until they’ve proven themselves.

But Plasma’s launch this week (September 25, 2025) was different. The numbers alone turned my head: they seeded roughly $2 billion in stablecoin liquidity on day one. That’s massive! And it wasn’t just empty hype or fly-by-night projects—Aave, Euler, Ethena, and Fluid were integrated at launch. That’s not your average chain debut. Those are serious names in DeFi, and they don’t just deploy on any new blockchain on a whim. To me, that signals something much more meaningful, and it’s shifted my risk framework. If Aave and Euler are here, I’m paying attention.

Why Plasma Caught My Eye

So what exactly is Plasma, and why am I talking about it? The short version: it’s a blockchain built specifically for stablecoins.

Now, that might not sound radical at first—after all, every chain supports stables. But here’s the difference. Ethereum was designed for smart contracts. Solana was built for high-speed transactions. Most chains are general-purpose blockchains, and stablecoins just happen to exist on top of them. Plasma flips the script. The entire chain is designed with stablecoins as THE primary asset.

Think about what that means. Stablecoins have quietly become the lifeblood of DeFi. They’re how most people store value in crypto, they’re the bridge for payments, they’re ideally the future of remittances and moving money globally, they’re the unit of account for trading, and they’re the foundation for earning yield. Having a chain where stablecoins aren’t just an add-on, but the centerpiece is kind of a big deal.

Who’s Behind Plasma

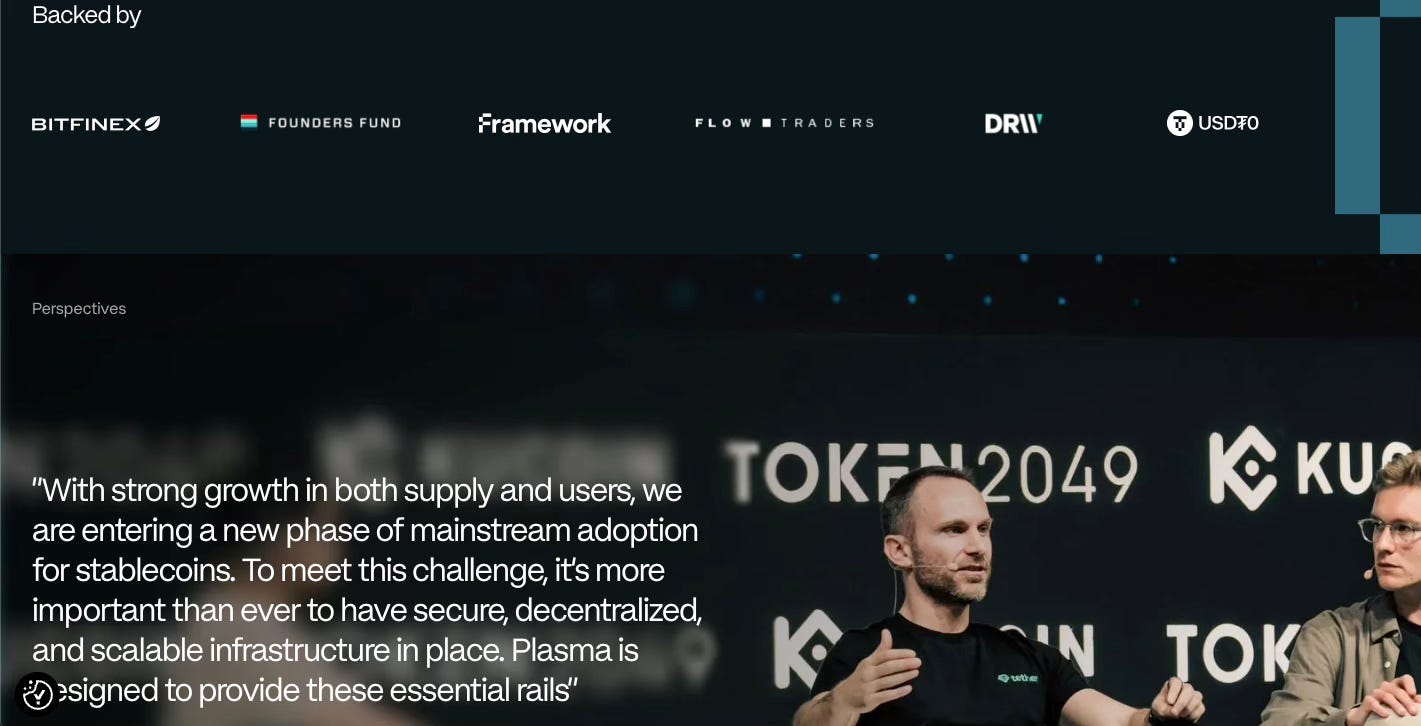

One thing I always look for when evaluating a new protocol or chain is the people behind it. Is it anonymous? Is there accountability? Are real builders with reputations at stake involved? In Plasma’s case, the team is out in the open. It was founded by Paul Faecks, and it’s backed by Tether and Bitfinex, with very public support from Tether CEO Paolo Ardoino. Earlier this year, Plasma raised $24 million to build out its mainnet, followed by a reported $373 million token sale. That’s not small potatoes—that’s serious capital.

And then you layer on the fact that from day one, names like Aave, Euler, and Ethena were live. To me, that combination of institutional backing and credible builders is rare for a chain this new. It tells me this isn’t just another experiment—it’s a serious attempt to create something lasting.

How Plasma Works in Practice

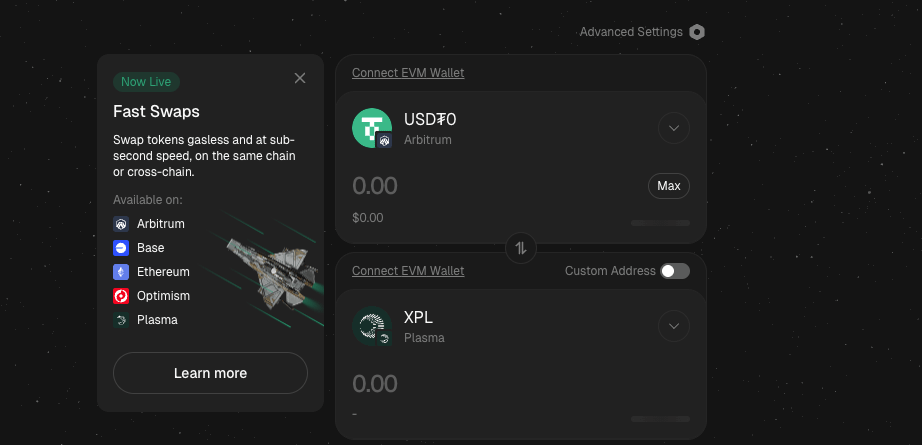

Plasma is EVM-compatible, meaning it works with Ethereum’s tooling and developer environment. That makes adoption easier for both developers and users who are already comfortable with MetaMask and the broader Ethereum ecosystem. Transactions require $XPL, the native gas token. In some cases, the system will auto-convert USDT for fees, which is a nice user-friendly feature, but it doesn’t always work seamlessly. In practice, you’ll want to keep a little XPL in order to interact with the blockchain.

You can purchase XPL on many major Centralized Exchanges, or you can use a bridge like Stargate to bridge and swap from another chain over to the Plasma Blockchain.

One feature Plasma has leaned into is zero-fee USDT transfers. That’s huge if you’re thinking about payments or just moving money around. It’s a subtle but powerful signal that they want this to be the chain where stablecoins actually circulate, not just sit in DeFi contracts.

Stable Lad Risk Grade

As exciting as Plasma’s launch has been, I have to keep my risk glasses on. New infrastructure always carries smart contract risk. Incentives are flowing heavily right now to attract liquidity, but those incentives will rotate. TVL can look impressive at launch but it’s always important to ask how much is sticky, and how much is just mercenary capital chasing rewards?

Then there’s the gas token issue. It sounds minor, but for usability, it matters. If you’re expecting auto-conversion to cover fees and it fails mid-transaction, that’s frustrating and risky. It’s not a dealbreaker, but it’s a detail that requires consideration.

So where does that leave me? Right now, I’m giving Plasma a B+ Grade! The plus is for the builders, the institutional backing, and the sheer momentum of the launch. The B is for the fact that it’s still brand new. The blockchain has not been truly battle-tested yet (although AAVE, Euler and other protocols certainly have, which is why the grade is a B and not lower). Over time, if Plasma proves resilient and grows consistently, that grade will improve quickly.

The Stablecoin Supercycle

Now, let’s zoom out. Plasma matters not just because it’s a new chain, but because of the bigger story happening around stablecoins. We’re in what is being called the stablecoin supercycle. Here’s what that means:

Tether just announced USA₮, a U.S.-regulated stablecoin, with Bo Hines tapped as CEO. That’s a major move, signaling Tether’s confidence in expanding into regulated markets.

Stablecoin issuers collectively hold over $120 billion in U.S. Treasuries, making them some of the largest holders of government debt in the world. That’s institutional-scale finance.

Stripe is rolling out USDC payments on Shopify, making stablecoin payments mainstream for e-commerce (there’s even a rumor going around that Stripe is planning on launching its own Stablecoin).

J.P. Morgan is piloting its JPMD deposit token on Base, a sign that even the largest banks are exploring tokenized dollars.

SWIFT is partnering with Consensys and major banks to build tokenized payment rails, which shows that the infrastructure of global money movement is shifting onto blockchains.

These are just a handful of the latest headlines, but when you put all that together, you realize stablecoins are no longer crypto’s sidekick. They’re becoming the superhero. And Plasma is launching right into the heart of this exact moment, as the first chain built entirely focused on stablecoins.

APYs and Early Incentives

Let’s not ignore the juicy part: the APYs. Right now, most of the yields on Plasma are above 10%. Not too shabby! Of course, those won’t last forever—high incentives at launch are designed to attract liquidity, and I expect they’ll remain volatile as Pendle (almost live on Plasma) and other major protocols begin offering their products on the blockchain. In any case it’s incredibly impressive to see how quickly liquidity is growing and how deep the markets already feel. TVL is climbing fast, and the activity looks real, not just numbers on a dashboard.

My Bottom Line

So where do I land on Plasma? It’s new, it’s not without risks, but it’s also one of the most interesting chain launches I’ve seen in a while. With $2 billion seeded on day one, backing from Tether, credible builders like Aave and Euler deploying instantly, and a vision centered squarely on stablecoins, Plasma is worth paying close attention to. For me, it’s already earned a place in my portfolio (see below full weekly portfolio update for paid subscribers).

The timing couldn’t be more perfect. As the stablecoin supercycle accelerates—with Tether expanding, Stripe integrating USDC, JPMorgan building deposit tokens, and SWIFT retooling global payments—Plasma is positioning itself as the blockchain built for this new era.

And that’s why I’m excited. Because stablecoins aren’t boring anymore. They’re the future of money on the internet.

Till next time,

The Stable Lad

Disclaimer: The content here is for educational purposes only. I’m not a licensed financial advisor, and nothing here should be taken as investment advice. Always do your own research, and never invest more than you can afford to lose. Stablecoins and DeFi carry risks, including potential loss of principal.